Article | Intelligent Investment

Business Insights | Geopolitical disruption: Pricing risk in a more volatile market

How geopolitical conflict is reshaping pricing, timing and execution risk and what it means for investors navigating Australia’s safe-haven appeal amid higher debt costs.

April 21, 2026

Explore CBRE’s quarterly Capital Markets magazine

Explore NowGeopolitical conflict has returned as a material force shaping global capital markets. For real estate, the impact will be partially sentiment driven, however the real impact is the repricing of cost, capital and risk in real time. Higher energy prices, rising bond yields and more expensive debt are lifting hurdle rates and compressing pricing tolerance. The result is not uniform, but an uneven market where value is being recalibrated by asset and sector.

Historically, major geopolitical shocks have not reliably derailed the economic cycle, but they do impact inflation and financing conditions, which is what matters most for real estate underwriting.

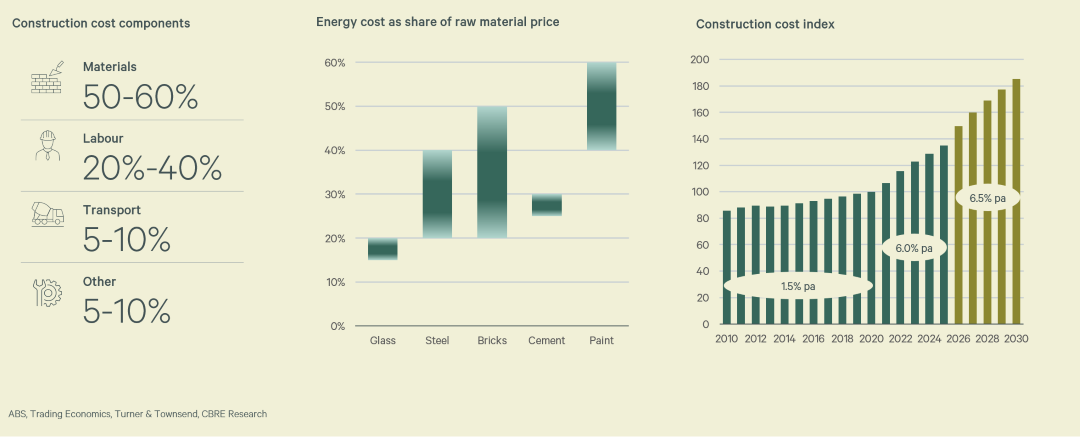

Heightened global tension is placing upward pressure on fuel, energy and materials, reinforcing an already elevated cost environment. These pressures flow directly into construction inputs, logistics and labour, lifting replacement costs and compressing development feasibility across sectors.

At the same time, higher bond yields and borrowing costs are already feeding through to pricing. As capital becomes more expensive, return expectations are resetting, driving price adjustment even where underlying asset performance remains sound.

Sameer Chopra, Head of Pacific Research for CBRE explains, “pre-2020s, construction was inflating at 1.5% per annum. It grew at 6% per annum over the past five years due to post-COVID demand/supply mismatch and Russia-Ukraine conflict. We expect 6.5% per annum average cost growth over 2026-2030, including an 18% spike over the next two years. Our early assessment is that economic rents will move 6% to 8% higher and new supply will become even more scarce.”

Andrew McCasker, Head of Debt & Structured Finance for CBRE, adds, “Lenders into the Australian market are still comfortable with the underlying fundamentals however there will be a stronger focus on consistency of cashflows and robustness to development feasibility as interest cost rise over the coming months.

Sector impacts: differentiated exposure, uneven outcomes

Office

Office markets are experiencing some of the most uneven outcomes of any sector.Pricing dispersion is being driven by asset quality and buyer conviction, with prime assets showing greater resilience than secondary stock. Higher bond yields have lifted required returns, which is likely to impact most assets in some form. At the same time, office supply pipelines are slowing materially across major CBDs, increasing the premium placed on assets that can capture future demand without significant execution risk.

This dynamic is widening the gap between buyer and seller expectations, particularly for secondary assets where timing and capital demand are most acute.

James Parry, Head of Office for CBRE Capital Markets, says: The geopolitical instability has had an immediate impact on the debt markets which reduces the probability of short-term yield compression; however occupier flight-to-quality, flight-to-value and flight-to-centralisation continues to push rent growth well in excess of current forecasts, across Australia and New Zealand. Whilst some buyers will opt to ‘wait and see’ how inflation and in turn debt markets plays out, others will seize the opportunity to invest while the investor sentiment is flat.

Industrial & Logistics

Industrial and logistics fundamentals remain supported by occupier demand, but feasibility is under pressure. Rising energy, transport and construction costs are flowing directly into steel, concrete and infrastructure inputs, lifting development costs and compressing margins.Lending appetite for the sector remains solid, reflecting confidence in long term demand. However, pricing discipline has tightened, particularly for developmentled strategies. The result is a market where demand remains supportive, but capital is more selective and returns are being recalibrated against a higher cost base.

Chris O’Brien, Head of Industrial & Logistics for CBRE Capital Markets, says: “Demand for industrial and logistics is still strong, but rising build, transport and energy costs are making projects harder to stack up. Investors and lenders are running more conservative numbers. We expect money to stay in the market, but it will be more selective, backing assets with secure income and strong WALEs that don’t rely on big cost assumptions.”

Retail

Retail performance is becoming increasingly asset specific, with income sustainability and future growth playing a central role in pricing outcomes.“The relative returns and recalibration in values for high-quality assets remain compelling, reinforced by market-adjusted income streams and robust tenancy performance, providing attractive inbuilt robust growth. The lack of recent and forecasted competing supply has been a key contributing factor to asset performance and investor demand,” explains Simon Rooney, Head of Retail for CBRE Capital Markets.

Lender appetite for retail assets is remaining relatively stable compared to other sectors, reflecting confidence in income backed assets despite higher base rates. However, higher bond yields are still influencing required returns, meaning price adjustment is occurring at an asset level rather than across the sector as a whole.

Core metropolitan located assets anchored by non-discretionary spending and strong covenants continue to attract significant interest, while secondary assets face greater scrutiny on pricing, capex requirements, and execution risk.

Living

Australia’s Living Sectors (build-to-rent, purpose-built student accommodation and co-living) are well positioned to benefit from heightened market uncertainty, given the defensive income characteristics and strong demand fundamentals underpinning completed assets.Completed living sector assets continue to demonstrate resilient occupancy and rental growth, supported by structural undersupply, population growth and the essential nature of rental accommodation. In the current environment, these assets offer highly visible cashflows and inflation-linked income growth, reinforcing their role as a core allocation for both domestic and offshore capital. Valuations are expected to remain comparatively stable as investors increasingly prioritise income security and operational performance.

While development markets are experiencing cost and financing pressures, these conditions are expected to constrain new supply rather than weaken fundamentals. Rising construction and financing costs are likely to delay some projects, tightening the delivery pipeline and reinforcing long-term rental growth prospects for existing stock. Investors with exposure to completed or near-complete assets are therefore positioned to benefit from continued demand imbalance and above-trend rental growth. Well located development projects with fixed price construction contracts will continue to attract capital support although investors are likely to require additional risk coverage in the feasibilities.

Andrew Purdon, Head of Living Sectors for CBRE Capital Markets, says: “In periods of geopolitical volatility, the Living sectors consistently demonstrate their defensive qualities. Completed assets are performing strongly, underpinned by high occupancy, sustained rental growth and a structural shortage of supply. As development pipelines decline, existing assets are positioned to capture the benefits of constrained new delivery and ongoing demand. Residential rental investments continue to offer some of the most resilient and transparent cashflows in real estate, and this profile is increasingly attractive to Australian and global investors seeking stability with long-term growth.”

Hotels

Hotels face indirect exposure to geopolitical disruption through air travel and diminished air capacity. Airspace restrictions across parts of the Middle East are having an effect on the number of international inbound travellers coming to Australia not only from the Middle east region, but also from the UK and Europe from travellers who typically use the Middle East as a transit point when coming to Australia. In addition, higher jet fuel prices are flowing through to airfares. This raises friction for international travel, particularly for price sensitive leisure demand.“This conflict is another reminder of how connected the world is in so many respects. There is an obvious direct link between air capacity to a destination, both domestic and international, and the performance of hotels in that destination. Increased airfare costs as a result of fewer international routes and higher jet fuel costs are likely to have a near term negative impact on demand.” Michael Simpson, Head of Hotels for CBRE Capital Markets says, “Positively, given approximately 75% of overnight visitor expenditure in Australia is from domestic tourists, we are somewhat cushioned from a reduction in international inbound.”

However, the impact on hotels is uneven. Assets with strong domestic demand, corporate travel and events exposure are more insulated, while destinations reliant on long haul international arrivals face greater sensitivity. At the same time, higher construction and financing costs are constraining new hotel supply, providing a degree of support for existing assets despite near term uncertainty.

Looking ahead

Looking ahead, geopolitical conflict is set to shape Australian real estate less through near-term leasing conditions, consumer demand and operating performance, and more through indirect means of energy-related inflation and increasing interest rates - lifting the returns investors require and tightening pricing tolerance, particularly for more leveraged strategies.Assets with durable income and a clear, fundable capex pathway will hold up better, while properties that require major upgrades, carry leasing risk or rely on more complex repositioning plans are more exposed to higher return hurdles.

“For buyers, the opportunity to look through the cycle and acquire high‑quality real estate that is typically unavailable has re‑emerged. This window looked to have closed earlier this year. For sellers, buyers will remain discerning therefore bidder depth will vary widely. Secondary assets are likely to continue to face challenges. Successful sales will require clear messaging and a structured, well‑executed sales process”

CBRE will continue to monitor and share updates as conditions evolve.

Get in Touch

Andrew McCasker

Head of Debt & Structured Finance – Capital Markets, Pacific

Chris O'Brien

Head of Industrial & Logistics – Capital Markets, Pacific

Simon Rooney

Head of Retail – Capital Markets, Pacific

Andrew Purdon

Head of Living Sectors – Capital Markets, Pacific

Michael Simpson

Head of Hotels – Capital Markets, Pacific

Pacific Real Estate Market Outlook 2026

Pacific Real Estate Market Outlook - April 2026 edition

Find out where the opportunities, risks and challenges will be for market activity and decision makers this year.

Read the Report